Most people in the biopharmaceutical industry recognize, at least anecdotally, that the use of disposables in biomanufacturing is moving forward. At BioPlan Associates, we’ve tried to quantify how things are advancing and capture some of the shifts in attitudes, especially in light of current economic challenges. The major shift is that decisions are being made more from an operational point of view. It’s become less a question of if disposables will be implemented than of where and how. Our newest industry study shows that concerns over adoption are rapidly becoming less strategic and more operational and commercial (1). As the “Methodology” box explains, this year’s study elicited data on 10 critical areas associated with biopharmaceutical production (disposables being one of these) from 443 production executives at drug developers and CMOs in 39 countries.

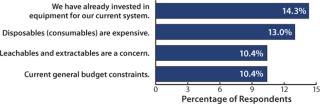

This year, decision makers’ objections to disposables have declined both in quantity and importance. For example, we asked respondents about their most important reasons for not increasing their use of disposables. Regulatory worries, such as how to treat leachables and extractables (L&E) issues, have consistently been near the top of that list. Last year, they were the number-one concern for 16.6% of biomanufacturers. This year, that percentage dropped to 10% (Figure 1). Also last year, a “lack of disposable equipment that meets process requirements” was a major concern, and this year it seems to have drifted into secondary status.

SURVEY METHODOLOGY

This sixth in the series of annual evaluations by BioPlan Associates, Inc. yields a composite view and trend analysis from 443 responsible individuals at biopharmaceutical manufacturers and contract manufacturing organizations in 39 countries. The methodology also included 140 direct suppliers of materials, services, and equipment to this industry. This year’s survey covers issues such as current capacity, future capacity constraints, expansions, use of novel expression systems, use of disposables, trends and budgets in disposables, trends in downstream purification, quality management and control, hiring issues, employment, and training. The quantitative trend analysis provides details and comparisons of production by biotherapeutic developers and contract manufacturing organizations (CMOs) and evaluates trends over time, assessing differences in the world’s major markets in the United States and Europe.

Trending toward Greater Acceptance

Trends suggest greater acceptance of single-use products. Three of the top four issues this year are cost or budget related rather than technical. The industry seems to have become comfortable enough with disposables that its key question now appears to be one of cost-effectiveness for specific applications.

In fact, the top concern (“We have already invested in equipment.”) suggests that decision makers are not against disposables per se, but rather they are not yet convinced that, for their applications, they need to change. They’re saying something like, “If it isn’t broken, why fix it?” Even here, though, the winds are shifting. This perception has dropped since last year from 19% of biomanufacturers down to 14% this year, which may indicate an increasing receptivity toward disposables even in current facilities.

The bigger the company, the less likely it is to be interested in implementing more disposables. When we asked whether respondents “agreed” or “strongly agreed” with such implementation, an average 51% of all respondents felt that “investment in current equipment” was restricting their use of disposable. Most large biomanufacturers (73.3%) indicated that investments in current equipment would inhibit their use of disposables to some degree — compared with only 49.5% of mid-tier companies.

Increased Adoption

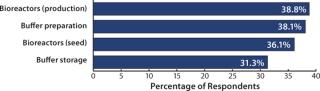

We’ve found that single-use products (especially the more technically advanced ones) are being adopted in new areas of biomanufacturing at an increasing rate. For example, production bioreactors were newly introduced to 39% of respondents’ facilities over the past 12 months (Figure 2). And somewhat surprising, 30% of large biomanufacturers introduced production bioreactors within their facilities during that time. These are likely to be smaller, development-scale bioreactors.

When we compare newly implemented disposables use in the United States and Western Europe, we find some significant differences. For example, 47% of US respondents indicated that they were currently using disposable production bioreactors (at some stage within their facility) compared with 28% in Western Europe. Seed-bioreactor use was consistent for both regions.

Newly implemented buffer storage is performed in disposables by 31.2% of US facilities compared with 39.6% of western European facilities and 16.7% of those elsewhere in the world. Buffer preparation is performed with disposables at 45.3% of US facilities and 35.9% of western European facilities. Mixing with disposable technologies is somewhat less common in the United States (12.5%) than in Western Europe (20.8%).

Reasons for Increasing Disposables Use

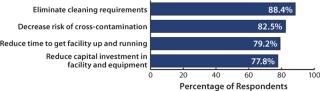

We identified 25 reasons that respondents considered to be factors in deciding on the implementation of single-use technologies. This year, the top reason continues to be to “eliminate cleaning requirements,” as noted by 88% as being important or very important (50% indicated it as very important both this year and last). Following were “decrease risk of product cross contamination” (83% this year, 78% last year), “reduce time to get facility up and running” (79% this year, 74% last year), and “reduce capital investment in facility and equipment” (78% this year, 73% last year).

Other Trends and Issues

Leachables and Extractables: We identified 26 possible reasons that manufacturers may be restricting their use of disposables. Topping the list — with >64% of our respondents indicating that they agree or strongly agree — was concern over L&E. The level of anxiety over this was higher than for other issues, but it was lower than the 75% response we saw last year.

Most manufacturers and vendors recognized that testing disposable devices for leachable and extractable contaminants in biomanufacturing is difficult, given the infinite variety of conditions such as contact times, pH, and myriad others. Given those difficulties, who should be doing the analysis and L&E testing? With 82% of our respondents indicating they agree that “vendors should generate L&E data and validate,” this suggests both a need and opportunity for those vendors. Although 47% of respondents indicated that they expected to generate their own L&E data for phase 3 or commercial applications, fully 22% indicated that they would pay 25% more for disposables if they came with useful, vendor-generated L&E data (in fact, 9% would pay 50% more).

Bag Breakage: Although the breakage of bags is no longer a critical issue to all, it was still cited by 63% of our respondents as a reason they might not increase disposables use. This is up from 55% last year — and up sharply from the previous two years’ surveys (44% for 2006, 35% for 2005).

Cost: The cost issues (noted by 61%) were raised with highest objections by our contract manufacturing respondents, 70% of whom agreed that cost of disposables (consumables) was their reason for restricting disposables use. This compares with 59% of biopharmaceutical sponsor/manufacturers.

Single-Vendor Dependence: Another trend limiting use of disposables was a fear of becoming too dependent on a single vendor (with 52% of respondents indicating this was a concern).

Collaborations Expanding Disposables Use

Industry collaborations are on the rise as organizations involved in single-use technology begin to realize they can’t do it alone. Some of these deals involve collaborative research, others involve standards setting, and others involve mergers. According to Kevin Ott, executive director of the Bio-Process Systems Alliance (BPSA), “Engineering firms and systems design houses, as well as some of the early-adopters of single-use products in biopharma are beginning to participate collaboratively. BPSA, as a trade organization, is a forum for suppliers, users and designers to discuss both hurdles and opportunities in the adoption of plastics-based bioprocessing.”

Ott has found that mergers and consolidations in the single-use supply chain are also on the rise. He notes that >80% of BPSA members were involved in a divestiture or acquisition over the past five years. “The January 2008, $27 million acquisition of LevTech by ATMI is a good example of both companies leveraging their existing expertise to expand globally,” he said. “Last month, TKMS [Turn-Key Modular Systems Inc.] acquired HyNetics LLC from Alfa-Laval to provide mixing systems in the 30- to 1,000-L range. Whether through collaborations or mergers, integrating company offerings and skill sets is a trend in single-use.”

As Pall Life Sciences’ senior vice president of scientific affairs (and chairman of BPSA), Jerold Martin agrees: “Single-use technology is still in the early stages of implementation. The pharmaceutical industry’s scientific and technical societies such as ASME, ISPE, and PDA, with encouragement from the BPSA, are working to provide end users, designers, suppliers, and regulators with consensus best-practice guides, standards, technical reports, and case studies on implementation of single-use processes. These professional communities are leveraging their diversity to provide keys for successful implementation and reduction of risk to this platform technology.”

The biotechnology industry is placing greater demands for faster, better, and cheaper biopharmaceuticals. Innovative products such as disposables, combined with the collaborative efforts within this industry, will help the bioindustry serve the demands of the global health-care system.

For more information visit:www. bioplanassociates.com